Also known as the income statement, the profit and loss Statement is the mother of all financial statements. The profit and loss statement (P&L) not only tracks the key revenue streams of a business but the areas of spend as well.

The profit and loss statement captures a business’ revenue and expenses over a specified time period (often a year). These two variables are then used to show if the business made a net profit or a net loss within that time frame. If the business’ revenue is greater than its expenses, then the profit and loss statement shows net profit. If the business’ revenue was less than its expenses, then the profit and loss statement shows a net loss.

Management will regularly track the P&L to monitor the health of the business and forecast how it will perform in the future. External investors and regulators also rely heavily on the P&L to judge how a business is doing and the choices being made at the company. The key elements are the revenue, or money coming in to the business, and then the expenses associated with that revenue. It is important to note that the P&L tracks when activity happens but not necessarily when cash is paid out. The goal is to align actions with impact and show the ability of a company to generate profit. This is different from the statement of cash flows which tracks actual movement of money.

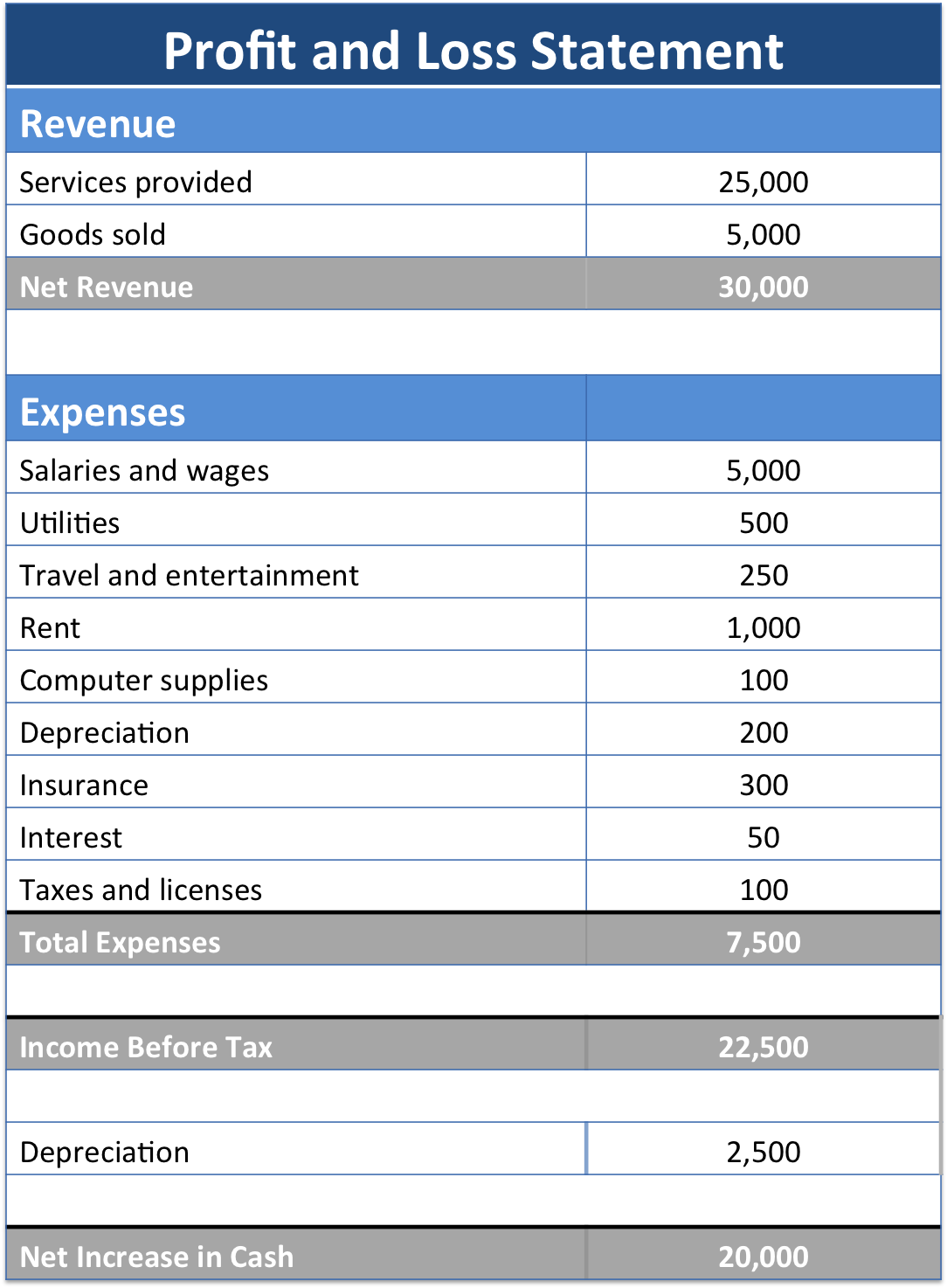

The table below provides a basic example of a profit and loss statement and the key elements it tracks.

As you can see, the profit and loss statement captures some very important aspects of a business’ operations. To learn more about other accounting fundamentals, head on over to our Accounting 101 page. Alternatively, see our database of accounting colleges to find the right accounting program for you.